Skip to content

About Us

Our Services

Tax News & Updates

Tax Calendar

Self-Employed/Employer Info

Contact

100% Deduction for Meals

Twitter

Facebook

LinkedIn

Email

Related Posts

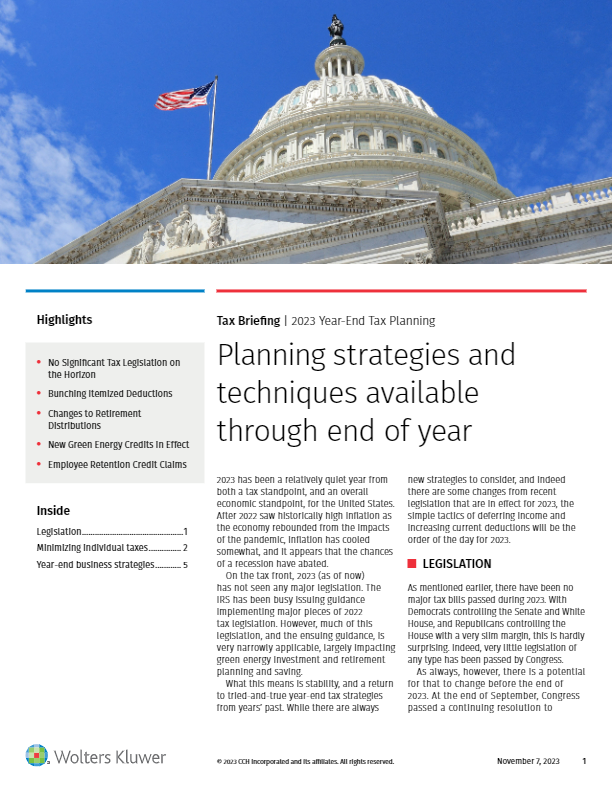

2023 Year-End Tax Planning

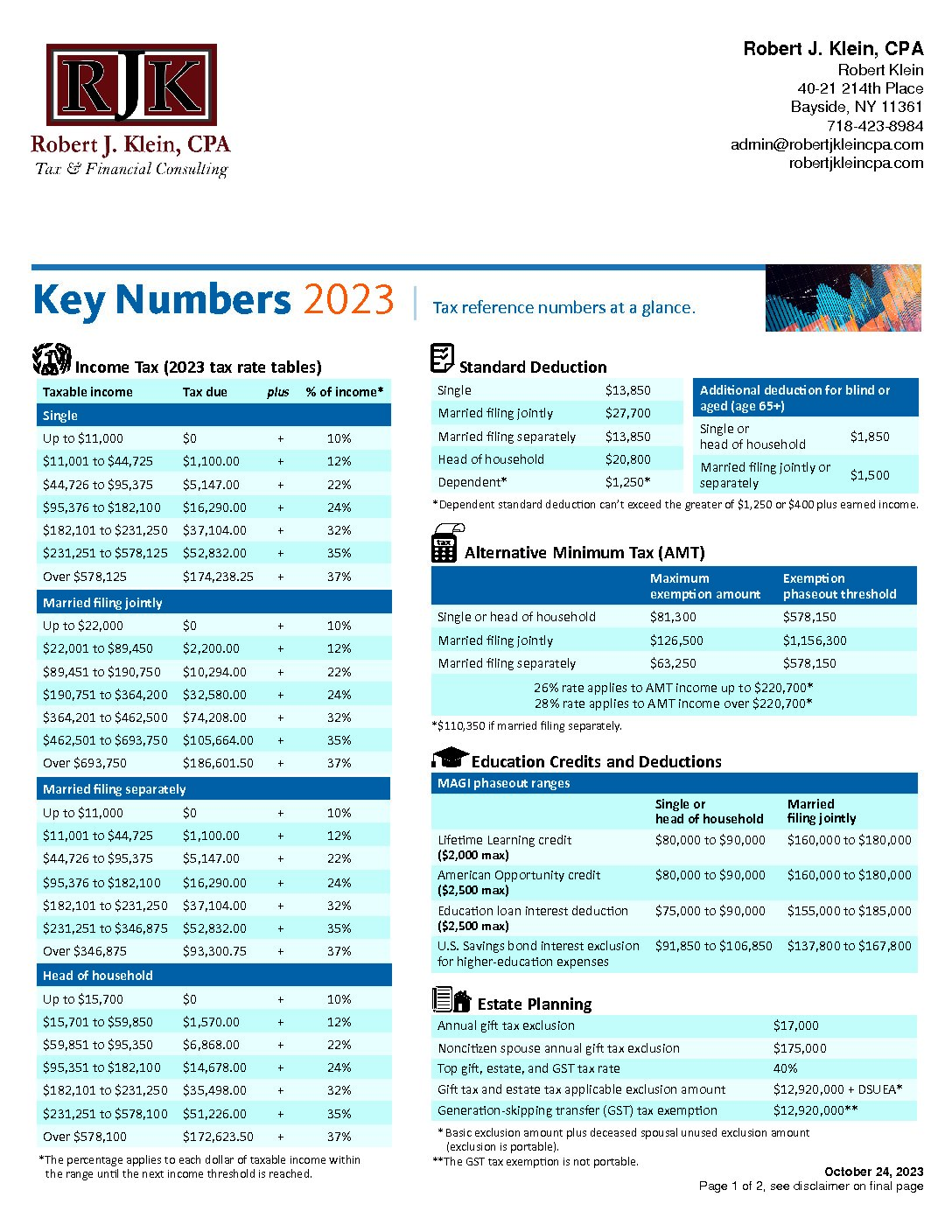

2023 Individual Income Tax Laws

Omnibus Bill, Secure 2.0 Act

2022 Year-End Tax Planning

Inflation Reduction Act

2022 Individual Income Tax Laws

2021 Year-End Tax Planning

2021 Individual Income Tax Laws

Enhanced Child Tax Credit 2021

American Rescue Plan Act of 2021

100% Deduction for Meals

Overview of Second Draw Loans for the Paycheck Protection Program

Overview of First Draw Loans for the Paycheck Protection Program

Covid-19 Retirement Plan Relief Measures

Required Minimum Distribution Age Change

Back To Top

Search

Submit